Category Archives: Others

Correspondent Banking: Issues and Current Initiatives

Correspondent banking services are essential for companies and individuals to transact internationally and make cross-border payments. Recently read a report “Cross-Border Interbank Payments and Settlements – Emerging Opportunities for Digital Transformation” which highlighted many issues related to existing cross border payments and how Central Banks around the world are working towards solving these problems.

This article highlights issues related to Cross Border payments from the perspective of Sender and Beneficiary, Commercial Banks and what initiatives are underway to solve those problems.

Continue reading Correspondent Banking: Issues and Current Initiatives

Unregulated Deposit Schemes Banned

Government issued an ordinance “The Banning of Unregulated Deposit Schemes Ordinance 2019” on 21 Feb 2019.

This article discusses what is deposit, what is regulated deposits scheme and unregulated deposit scheme, what is banned and what is not banned, from when is the Ordinance applicable, to whom, List of Regulated Deposit Scheme and FAQ

PNB scam fallout: Outstanding buyers’ credit shrinks by $25 b

The Hindu Business Line Published our report on Buyers Credit Outstanding going down by $25 Billion on today’s front page.

Published with Approval: Original Article Link

Continue reading PNB scam fallout: Outstanding buyers’ credit shrinks by $25 b

Buyers Credit Outstanding Down by $25 Billion

Since RBI Stopped Buyers Credit Transactions against LOU and LOC, few questions kept on coming up regularly

- What was the outstanding amount of buyers credit in overseas branches of Indian Bank as RBI data did not provide bifurcation products wise ?

- What is the run down in books of these bank since 13 March 2018 RBI Circular ?

- What is its impact on Libor based finance available to Indian importers ?

In this article we have provided the data and analysis which will answer the first two questions.

Continue reading Buyers Credit Outstanding Down by $25 Billion

Why are Indian Banks Closing Overseas Branches ?

Indian Banks have closed 37 Overseas branches till date and another 60 – 70 branches are under review. This article gives an overall summary of Indian banks presence internationally, reason for reducing number of branches and bankwise update on branches closed or in process of closing.

Continue reading Why are Indian Banks Closing Overseas Branches ?

Reserve Bank’s decision to ban LoUs will badly Impact SME

Reserve Bank’s decision to ban LoUs is a knee-jerk reaction; can backfire badly, warn traders

Article in firstpost.com printed with permission:

An industry-wide practice that worked well until the end of business hours on Tuesday, which allowed D Dhanasekaran’s Tiruppur-based textiles firm — Abi Tex Mills — import machinery from Oman and boost production, has now gone haywire with the Reserve Bank of India’s (RBI) decision to bar banks from issuing guarantees in the form of letters of undertaking (LoUs) and letters of comfort. “My machinery took a year to be imported and has been installed in the factory for a few months now. But now with buyer’s credit cancelled, I am focused on how to make payments instead of my production,” Dhanasekaran said.

Continue reading Reserve Bank’s decision to ban LoUs will badly Impact SME

Reuters: Indian importers face funding crunch with clampdown on credit guarantees

Indian Banks adds Additional Control to SWIFT System

As per Government of India revert in Rajya Sabha, PNB has taken below steps to ensure that such unauthorised activities in SWIFT systems are not repeated (other banks may have changed accordingly):

Continue reading Indian Banks adds Additional Control to SWIFT System

Bank Audit – Buyers Credit and Nostro Account

A bank branch goes through four kinds of audits and inspection

- Internal audit (done by bank staff) on regular basis

- Concurrent audit (done by a third party), on monthly or quarterly basis

- Statutory audit (done by the statutory auditor) on quarterly basis

- Inspection by RBI (annual basis).

In relation to buyers credit transaction, below are the few audit point which are covered by above audits.

Continue reading Bank Audit – Buyers Credit and Nostro Account

Nimo Fallout on Import

The Telegraph has quoted me in the below article related to PNB scam impact on buyers credit: Article: “Nimo Fallout on Imports”

Implication on Buyers Credit because of PNB Fraud

Latest Articles:

- RBI Stops Buyers Credit Transactions (LOU & LOC)

- Indian Banks adds Additional Control to SWIFT System

- Bank Audit – Buyers Credit and Nostro Account

This article gives layman summary of the PNB fraud case and its impact on buyers credit product and various stake holders like Indian Bank Overseas Branches, Local Banks in India and Importers.

Continue reading Implication on Buyers Credit because of PNB Fraud

EU list of Non-Cooperative Jurisdictions : No Impact on Buyers Credit

On 5 December 2017, European Union (EU) Council approved and published a list of non-cooperative jurisdictions. Criteria used were:

- Tax Transparency

- Fair Taxation

- Implementation of Anti – BEPS (Base Erosion and Profit Shifting) standards

Continue reading EU list of Non-Cooperative Jurisdictions : No Impact on Buyers Credit

Post Libor World – Impact on Buyers Credit

In earlier article we have discussed about various aspect of Libor and its Impact on buyers credit transaction.

In brief, Libor attempts to answer a fundamental question: What is the cost of money? It does this for a range of currencies (dollars, euros, pounds, etc.) and for a range of maturities.

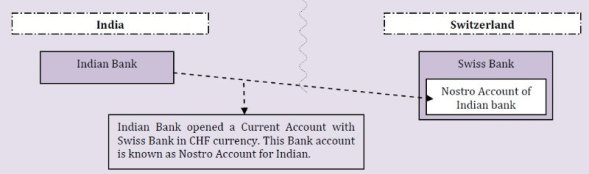

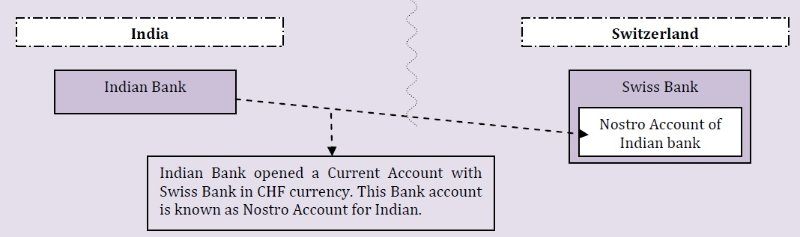

Nostro Account and Buyers Credit

What is Nostro Account ?

Subsidy under CLCSS Cannot be Claimed Where Buyers Credit is Availed

Trigger for this topic is a question that a reader asked:

“MSME manufacturing unit doing expansion of machinery by purchasing machinery from abroad get credit linked capital subsidy scheme (CLCSS) from Central Government.

MSME unit avails buyers credit for payment to overseas buyer and sanctioned term loan is not utilised . Can the unit be eligible for subsidy? ”

Below article gives basic details about Credit Linked Capital Subsidy Scheme and revert to above query.

Continue reading Subsidy under CLCSS Cannot be Claimed Where Buyers Credit is Availed

Permitted Methods of Import Payment

The trigger for this topic is a question that a reader asked:

Since Foreign Trade Policy allows imports in INR (Indian Rupees) also, what are the regulations related to buyer’s credit in respect of an import invoice which is in INR ?

Above question is more of an academic question as INR denominated import transaction are very limited but it will help in throwing light on concept of permitted methods of import payment.

Relationship Management Application (RMA) and Buyers Credit

Using Swift Codes Banks and Financial Institutions send and receive swift messages. But there must have been times where you might have come across your bankers coming back to you stating that they do not have swift key arrangement with buyers credit bank. Thus they will not be able to send Letter of Undertaking (LOU) / Letter of Comfort (LOC) authenticated swift message (MT799) to buyers credit bank. Below article gives a brief about why situation arise.

Continue reading Relationship Management Application (RMA) and Buyers Credit

Five Years of Leading the RBI – Looking Ahead by Looking Back

On 29 August 2013 Dr. D Subbarao Governor, Reserve Bank of India delivered the attached speech on occasion of Tenth Nani A. Palkhivala Memorial Lecture at Mumbai.

On 29 August 2013 Dr. D Subbarao Governor, Reserve Bank of India delivered the attached speech on occasion of Tenth Nani A. Palkhivala Memorial Lecture at Mumbai.

It is a candid speech with lot of insights.

Speech: Five Years of Leading the RBI – Looking Ahead by Looking Back

Myanmar Economic Sanctions – Background, Recent Relaxation & Trade Finance

Myanmar has been under various international economic sanction for more than a decade, which has crippled its international trade. Below article gives a background of economic sanctions on Myanmar, recent relaxations in these sanctions and what will be its likely impact on trade finance from Indian importers perspective.

Continue reading Myanmar Economic Sanctions – Background, Recent Relaxation & Trade Finance

Impact of Libor Review on Trade Finance in India

Note: Since this article was written, below regulation has been implemented. Refer Article: Change in LIBOR Tenures and Impact on Trade Finance

Continue reading Impact of Libor Review on Trade Finance in India

Pushing the reset button on LIBOR – Speech by Martin Wheatley

Note: Since this article was written, below regulation has been implemented. Also Refer Article: Change in LIBOR Tenures and Impact on Trade Finance

Mr. Martin Wheatley – Managing Director, FSA, and CEO Designate, FCA – gave a speech at the Wheatley Review of LIBOR. It contain details on various issues in relation to LIBOR and his final recommendation of rectifying the same. It is worth reading, thus sharing with you complete speech below.

Continue reading Pushing the reset button on LIBOR – Speech by Martin Wheatley

Basel III – Future Impact of Trade Finance

The Basel Committee on Banking Supervision (BCBS, or Basel Committee) is an institution created by the central bank Governors of 27 members from both developed and emerging economies. The most influential publications by the BCBS are Basel Accords. The key part of Basel framework as commonly referred to, guides banking industry how to calculate risk-weighted assets (RWA) and capital requirements. The Basel Committee gave its final text of Basel III on Dec 2010 of details of updated global regulatory standards on bank capital adequacy and liquidity, which was agreed by the Governors and Heads of Supervision, and endorsed by the G20 Leaders at their November 2010 Seoul summit.

Suppliers Credit or Buyers Credit is not available for Merchanting Trade

Post below articles, guidelines have been revised. Please refer article “Revised Guidelines for Merchanting / Intermediary Trade“

Continue reading Suppliers Credit or Buyers Credit is not available for Merchanting Trade

IMO Number and Its importance in case of Buyers Credit

What is IMO Number ?

The IMO ship identification number is made of the three letters “IMO” followed by the seven-digit number assigned to all ships by IHS Fairplay when constructed. This is a unique seven digit number that is assigned to propelled, sea-going merchant ships of 100 gross tons and above. It serves the purpose of identifying ships. It is a Unique number which does not change, even if when the ship’s owner, country of registry or name changes.

Continue reading IMO Number and Its importance in case of Buyers Credit

OFAC Countries & Implication on Buyers Credit

What is OFAC Sanctions ?

- The Office of Foreign Assets Control (OFAC) is an office of the Treasury Department of United States of America (US).

- OFAC administers and enforces economic and trade sanctions based on U.S. foreign policy and national security goals against targeted foreign countries, organizations, entities, and individuals.

- Regulations issued under Trading With the Enemy Act (50 U.S.C. App.§§ 1-44) or by the US President under authority delegated under the International Emergency Economic Powers Act.

- The OFAC sanctions programs are implemented through restrictions on imports and exports, prohibitions on financial transactions, freezing of assets, and other means.

Continue reading OFAC Countries & Implication on Buyers Credit

Buyers Credit All-In-Cost Ceiling may move back to L+200bps from 01/04/2012

In its Circular dated 15/11/2011, RBI had increased the all-in-cost ceiling for Buyers Credit from 6 Month L+ 200 bps to 6 Month L + 350 bps subject to condition that is only upto 31/03/2012 and after subject to review there after.

Continue reading Buyers Credit All-In-Cost Ceiling may move back to L+200bps from 01/04/2012

LIBOR Rates: Brief, History, Currencies, Maturities

Post below article there has been change in Libor Guidelines. Refer article “Impact of Libor Review on Trade Finance in India” & “Pushing the reset button on LIBOR – Speech by Martin Wheatley“

LIBOR in brief

LIBOR stands for London InterBank Offered Rate. LIBOR is an indicative average interest rate at which a selection of banks (the panel banks) are prepared to lend one another unsecured funds on the London money market. Although reference is often made to the LIBOR interest rate, there are actually 37 different LIBOR interest rates. LIBOR is calculated for 7 different maturities and for 5 different currencies. The official LIBOR interest rates (bbalibor) are announced once a day at around 11:45 a.m. London time by Thomson Reuters on behalf of the British Bankers’ Association (BBA).

Continue reading LIBOR Rates: Brief, History, Currencies, Maturities