Income Tax Return Form – ITR-4 (Sugam) is applicable to Resident Individuals, HUFs and Firms (other than LLP) having total income upto Rs. 50 Lakh and having Presumptive Business Income under sections 44AD or Presumptive Income from Profession under section 44ADA or Presumptive Income from Goods Carriages under section 44AE.

The new ITR-4 form is not applicable to:

- Non-residents and Residents but not ordinarily resident (RNOR)

- An individual who is either Director in a company or has invested in unlisted equity shares

- Business Code – 09005 – General commission agents, commodity brokers and auctioneers is not available in new ITR-4 Sugam.

The major changes in ITR – 4 applicable for the Assessment year 2019-20; Financial year 2018-19 are as below:

1. Filing Status:

New insertions :

- Whether this return is being filed by a representative assessee? If Yes, then Name, Address, PAN and Capacity of the representative as Legal Heir, Manager, Guardian or Other needs to be provided.

- Field for Nature of Employment has been added whether Govt, PSU, Pensioners or Others.

Fields like Income Tax Ward / Circle, Whether Person governed by Portuguese Civil Code, Enter PAN of Spouse if applicable, Residential Status and Tax Status have been removed.

2. Part B Gross Total Income:

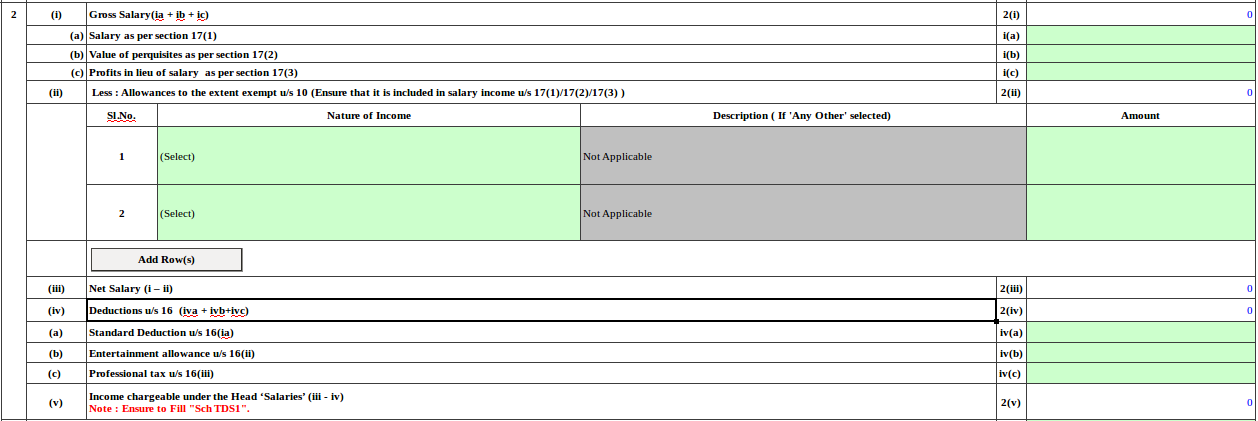

A. Income from Salary – Item No. 2:

In the new form salary income disclosure is required as per Form 16 under below heads:

- Gross Salary

- Salary as per section 17(1)

- Value of perquisites as per section 17(2)

- Profits in lieu of salary as per section 17(3)

- Less : Allowances to the extent exempt u/s 10 (included in salary income above). Select from the list given for Nature of Exempt allowance. Provide Description If ‘Any Other’ is selected for Exempt Allowance.

- Deduction u/s 16

- Standard Deduction u/s 16(ia)

- Entertainment Allowance u/s 16(ii)

- Professional Tax u/s 16(iii)

B. Income from House Property – Item No. 3 vi:

New insertion : Arrears/Unrealized Rent received during the year Less 30% under Income from House Property.

C. Income from Other Sources – Item No. 4:

Earlier only amount under Income from Other Sources was required to be furnished, now specific details under below heads are required:

- Nature of Income from the list provided below is to be selected and amount is to be mentioned.

- Interest from Saving Account

- Interest from Deposit (Bank / Post Office / Co operative Society)

- Interest from Income Tax Refund

- Family Pension

- Any Other.

- Description is to be given If ‘Any Other’ is selected. For Example Tailoring income.

- In case the nature of other sources income is selected as Family pension then a new row has been inserted as :

- Less: Deduction u/s 57(iia) (In case of family pension only).

3. Part C – Deductions and Taxable Total Income:

Headings of Various deduction sections from 80C to 80U has been clearly specified.

- Section 80D has been further sub classified under:

- a) Health insurance premium – Maximum limit Rs. 1,00,000.

- b) Medical expenditure – Maximum limit Rs. 1,00,000.

- c) Preventive health check-up – Maximum limit Rs. 5,000.

- Section 80DDB – Medical treatment of specified disease :

- Self or dependent – Maximum limit Rs. 40,000.

- Self or dependent-Senior Citizen – Maximum limit Rs. 1,00,000.

- Section 80QQB – Royalty income of authors of certain books has been removed.

- Section 80RRB – Royalty on patents has been removed.

- Section 80TTA – has been changed to Interest on deposits in saving bank Accounts from Income from Interest on saving bank Accounts.

- New Section 80TTB – Interest on deposits in case of senior citizens has been inserted – Item no. 6p : Deduction shall be allowed from amount in “Income from Other Sources”

4. Health and Education Cess – Item No 11:

Health and Education Cess @ 4% on Tax Payable after Rebate

5. Details of Income From Business or Profession:

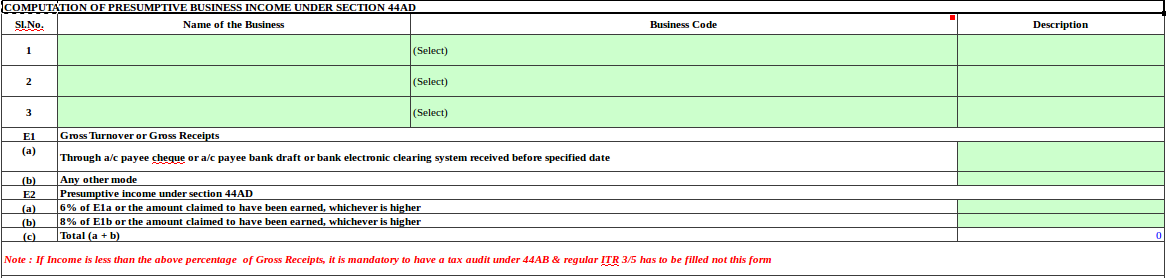

A. Computation of Presumptive Business Income under Sec 44AD:

New insertions :

- Name of the Business (Tradename / Firm Name)

- Business Code – Choose the business activity from the Nature of Business Code from code 01001 to 22001. Please note following codes are not available under this head : 09005 – General commission agents, commodity brokers and auctioneers; 14001 – Software development; 14002 – Other software consultancy; 14003 – Data processing; 14004 – Database activities and distribution of electronic content; 14005 – Other IT enabled services; 14006 – BPO services; 14008 – Maintenance and repair of office, accounting and computing machinery; 16001 – Legal profession; 16002 – Accounting, book-keeping and auditing profession; 16003 – Tax consultancy; 16004 – Architectural profession; 16005 – Engineering and technical consultancy; 16007 – Fashion designing; 16008 – Interior decoration; 16009 – Photography; 16011 – Business brokerage; 16013 – Business and management consultancy activities; 16018 – Secretarial activities; HEALTH CARE SERVICES – 18001 – General hospitals; 18002 – Specialty and super specialty hospitals; 18003 – Nursing homes; 18004 – Diagnostic centers; 18005 – Pathological laboratories; Medical professionals – 18010 – Medical clinics; 18011 – Dental practice; 18012 – Ayurveda practice; 18013 – Unani practice; 18014 – Homeopathy practice; 18015 – Nurses, physiotherapists or other para-medical practitioners; 18016 – Veterinary hospitals and practice; 18017 – Other healthcare services; 20010 – Individual artists excluding authors; 20011 -Literary activities; 20012 – Other cultural activities n.e.c.

- Description

B. Computation of Presumptive Income from Professions under Section 44ADA:

New insertions :

- Name of the Business (Tradename / Firm Name)

- Business Code – Choose the profession from the Nature of Business Code from code 14001 to 20012.

- Please note only below codes are available under this head : 14001 – Software development; 14002 – Other software consultancy; 14003 – Data processing; 14004 – Database activities and distribution of electronic content; 14005 – Other IT enabled services; 14006 – BPO services; 14008 – Maintenance and repair of office, accounting and computing machinery; 16001 – Legal profession; 16002 – Accounting, book-keeping and auditing profession; 16003 – Tax consultancy; 16004 – Architectural profession; 16005 – Engineering and technical consultancy; 16007 – Fashion designing; 16008 – Interior decoration; 16009 – Photography; 16011 – Business brokerage; 16013 – Business and management consultancy activities; 16018 – Secretarial activities; HEALTH CARE SERVICES – 18001 – General hospitals; 18002 – Specialty and super specialty hospitals; 18003 – Nursing homes; 18004 – Diagnostic centers; 18005 – Pathological laboratories; Medical professionals – 18010 – Medical clinics; 18011 – Dental practice; 18012 – Ayurveda practice; 18013 – Unani practice; 18014 – Homeopathy practice; 18015 – Nurses, physiotherapists or other para-medical practitioners; 18016 – Veterinary hospitals and practice; 18017 – Other healthcare services; 20010 – Individual artists excluding authors; 20011 -Literary activities; 20012 – Other cultural activities n.e.c.

- Description

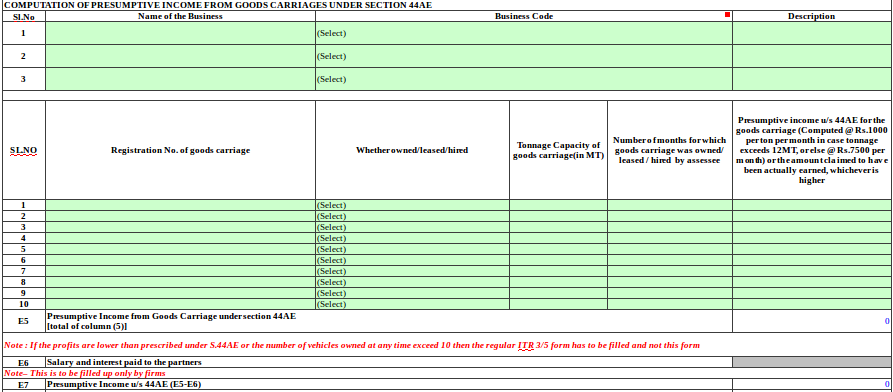

C. Computation of Presumptive Income from Goods Carriages under Section 44AE:

Schedule 44AE has been replaced by Presumptive Income From Goods Carriages U/S 44AE and is now part of Schedule BP

New insertions :

- Name of the Business (Tradename / Firm Name)

- Business Code – Choose from the list of Nature of Business Code from code 08001, 11002, 11008, 11010, 11011, 11012 and 11015.

- Description

- Registration No. of goods carriage

- Whether owned/leased/hired

- Tonnage Capacity of goods carriage(in MT)

- Number of months for which goods carriage was owned/ leased / hired by assessee

- Presumptive income u/s 44AE for the goods carriage (Computed @ Rs.1000 per ton per month in case tonnage exceeds 12MT, or else @ Rs.7500 per month) or the amount claimed to have been actually earned, whichever is higher

- Less: Salary and interest paid to the partners

D. Information Regarding Turnover/Gross Receipt Reported for GST

- GSTIN No.(s)

- Annual Value of Outward Supplies as per the GST Returns Filed

6. Details of Tax Deducted at Source:

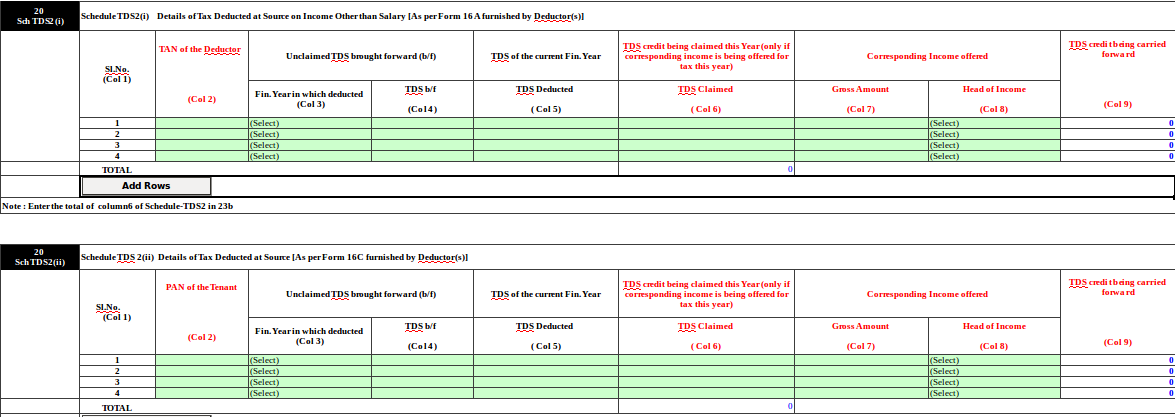

a. Item No. 20 Sch TDS 2(i) Details of Tax Deducted at Source on Income Other than Salary [As per FORM 16 A issued by Deductor(s)] and

b. Item No. 20 Sch TDS 2(ii) Details of Tax Deducted at Source [As per Form 16C furnished by the Deductor(s)] have been completely changed. New TDS Schedule needs below details:

- TAN of the Deductor / PAN of the Tenant

- Unclaimed TDS brought forward (b/f) – Fin. Year in which deducted , TDS amount b/f

- TDS of the current Fin. Year – TDS Deducted

- TDS credit being claimed this Year (only if corresponding income is being offered for tax this year) – TDS Claimed

- Corresponding Income offered – Gross Amount, Head of Income – Income from Business and Profession, Income from House Property, Income from Other Sources and Exempt Income.

- TDS credit being carried forward

Old Column for TDS credit in the name of, Name of the Deductor / Name of the Tenant, Unique TDS Certificate No., Tax deducted and Amount claimed in the hands of spouse as per section 5A or any other person as per rule 37BA(2), have been removed.

7. Details of Advance Tax and Self Assessment Tax Payments:

Item No. 21 Sch IT: Enter all the Advance tax and Self-Assessment tax details.

8. Details of Tax Collected at Source:

Item No. 22 Sch TCS: Details of Tax Collected at Source [As per FORM 27D issued by the Collector(s)] : Column for amount claimed in the hands of spouse, if section 5A is applicable, has been removed.

9. Bank Account Details of Non resident has been removed – Item No. 28(ii)

Field for Non-residents, who are claiming income-tax refund and not having bank account in India may, at their option, furnish the details of one foreign bank account has been removed.

10. Verification:

- System Date will automatically get picked in Date column.

- Difference of Submission Date and Verification Date

Submission Date is available in the ITR-V / Acknowledgement generated after submission of return. Verification date is the date of Receipt of ITR -V at CPC. In case of e-verification, it is available in the Acknowledgement.

11. Schedule AL:

Schedule for disclosure of Asset and Liability at the end of the year has been removed.

12. Schedule 80G:

Amount of Donation is to be shown separately as Donation in cash and Donation in other mode = Total Donation