Earlier articles “Major Changes in New ITR 1 ” & “Major Changes in New ITR 4” discussed about changes in respective forms.

One of the field in ITR forms requires details of Tax deducted at Source (TDS) during the year and brought forward of earlier years.

This article is about now to fill TDS columns in ITR 1 and ITR4.

Documents Required

Before filling up TDS details keep below documents for quick reference:

- Form 16 issued by employer

- Form 16A issued by deductor (e.g. Banks for TDS on Interest paid, Vendors)

- Form 26 AS

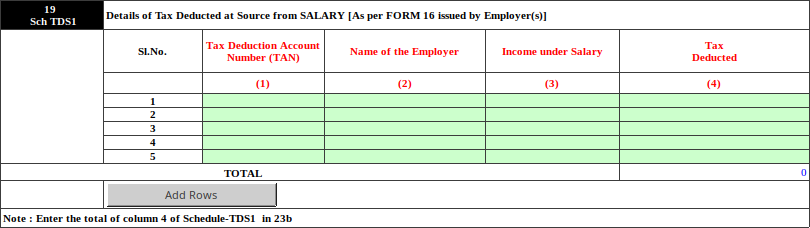

ITR 1 Sahaj : Tax Details

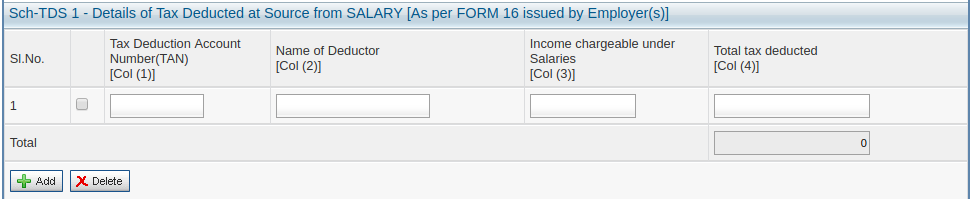

Sch- TDS1 :

Details of Tax Deducted at Source from Salary [As per FORM 16 issued by Employer(s)]

- Column (1) Tax Deduction Account Number (TAN)

- Column (2) Name of Deductor

- Column (3) Income chargeable under Salaries

- Column (4) Total Tax deducted

Add button is to be used in case of adding more than one employer.

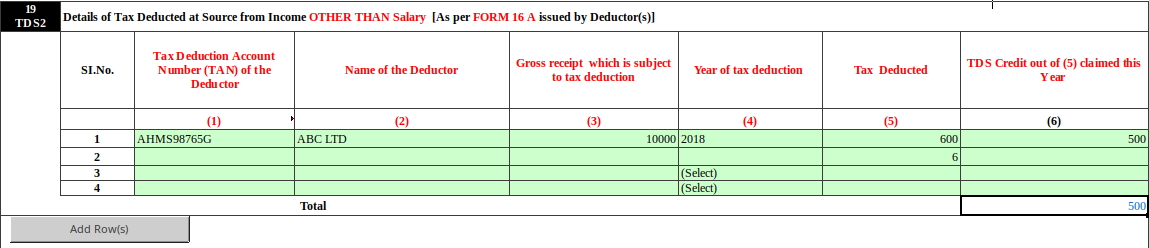

Sch- TDS2 :

Details of Tax Deducted at Source from Income OTHER THAN Salary [As per FORM 16 A issued by Deductor(s)]

- Column (1) TAN of Deductor

- Column (2) Name of Deductor

- Column (3) Gross receipt which is subject to tax deduction is to be provided.

- Column (4) Year of Tax Deduction – 2018

- Column (5) Amount of Tax Deducted (as per 26 AS) pre filled.

- Column (6) TDS Credit out of (5) claimed this Year is to be provided – It means out of the total tax deducted for the relevant year 2018-19, how much is to be claimed in this assessment year. Cases where full TDS is to be claimed then TDS Credit out of 5 claimed this Year in Column 6 will be same as Column 5.

Example 1: Where Full TDS is Claimed

TDS deducted in FY 2018-19 shown in 26 AS is Rs. 200. Out of which TDS pertaining to FY 2018-19 is Rs. 200. In this situation amount in column (5) Tax Deducted will be Rs. 200 and TDS credit in column (6) will be Rs. 200.

Example 2: Where TDS is Carried Forward to Next Year

TDS deducted in FY 2018-19 shown in 26 AS is Rs. 600. Out of which TDS pertaining to FY 2018-19 is Rs. 500 and for FY 2019-20 is Rs. 100. In this situation amount in column 5 will be Rs. 600 and column 6 will be Rs. 500. Hence TDS of remaining Rs. 100 will be allowed to carried forward in next year.

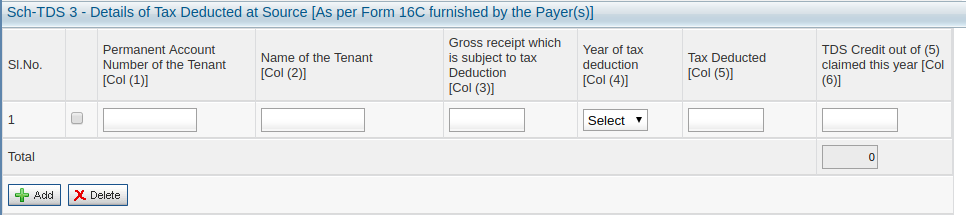

Sch- TDS3 :

Details of Tax Deducted at Source [As per Form 16C furnished by the Payer(s)] :

- Column (1) PAN of Tenant

- Column (2) Name of Tenant

- Column (3) Gross receipt which is subject to tax deduction is to be provided.

- Column (4) Year of Tax Deduction – 2018

- Column (5) Amount of Tax Deducted

- Column (6) TDS Credit out of (5) claimed this Year is to be provided – It means out of the total tax deducted for the relevant year 2018-19, how much is to be claimed in this assessment year. The remaining amount is allowed to be carried forward in future years.

ITR 4 Sugam : Tax Details

Sch TDS 1 :

Details of Tax Deducted at Source from SALARY [As per FORM 16 issued by Employer(s)]

- Column (1) Tax Deduction Account Number (TAN)

- Column (2) Name of Employer

- Column (3) Income under Salary

- Column (4) Tax deducted

Add button is to be used in case of adding more than one employer.

Sch TDS 2(i) :

Details of Tax Deducted at Source from Income Other than Salary [As per Form 16 A issued by Deductor(s)]

- Column (2) TAN of the Deductor

- Unclaimed TDS brought forward (b/f) of earlier years:

- Column (3) Financial year in which deducted (e.g. 2017 pertains to financial year 2017-2018)

- Column (4) Amount of TDS b/f brought forward of earlier years

- Column (5) TDS Deducted : TDS of the current Fin. Year (as per 26 AS) pre filled.

- Column (6) TDS Claimed : TDS credit being claimed this Year (only if corresponding receipt is being offered for tax this year) – TDS amount credit out of (5) claimed this Year is to be provided.

It means out of the total tax deducted for the relevant year 2018-19, how much is to be claimed in this assessment year. The remaining amount is allowed to be carried forward in future years.

Example 1: Where Full TDS is Claimed

TDS deducted in FY 2018-19 shown in 26 AS is Rs. 200. Out of which TDS pertaining to FY 2018-19 is Rs. 200. In this situation amount in column (5) Tax Deducted will be Rs. 200 and TDS credit in column (6) will be Rs. 200.

Example 2: Where TDS is Carried Forward to Next Year

TDS deducted in FY 2018-19 shown in 26 AS is Rs. 600. Out of which TDS pertaining to FY 2018-19 is Rs. 500 and for FY 2019-20 is Rs. 100. In this situation amount in column 5 will be Rs. 600 and column 6 will be Rs. 500. Hence TDS of remaining Rs. 100 will automatically come in column 9. It will be allowed to carried forward in next year.

Example 3: Where Last Years Unclaimed TDS is Claimed This Year

Unclaimed TDS brought forward from earlier years and claimed this year is Rs. 100. In this situation column 3 (Fin. year in which deducted) will be 2017, amount in column 4 will be Rs. 100 and column 6 will be Rs. 100.

Error Message

Error message 6 cannot be greater than 4 or 5 means: Fill amount either in column 4 & column 6 or in column 5 & column 6.

Corresponding Receipt offered:

- Column (7) Gross Amount pertaining to FY 2018-19 (Gross receipt on which TDS is deducted)

- Column (8) Head of Income out of Income from business and Profession, Income from House Property, Income from Other Sources or Exempt Income

- Column (9) TDS credit being carried forward to next year.

Sch TDS 2(ii) :

Details of Tax Deducted at Source [As per Form 16C furnished by the Payer(s)] :

- Column (2) PAN of the Tenant

- Unclaimed TDS brought forward (b/f) of earlier years:

- Column (3) Financial year in which deducted (e.g. 2017 pertains to financial year 2017-2018)

- Column (4) Amount of TDS b/f brought forward of earlier years

- Column (5) TDS Deducted : TDS of the current Fin. Year (as per 26 AS) pre filled.

- Column (6) TDS Claimed : TDS credit being claimed this Year (only if corresponding receipt is being offered for tax this year) – TDS amount credit out of (5) claimed this Year is to be provided. It means out of the total tax deducted for the relevant year 2018-19, how much is to be claimed in this assessment year. Cases where full TDS is to be claimed then TDS Credit out of 5 claimed this Year in Column 6 will be same as Column 5 ie Rs.200. Last Column – TDS credit being carried forward.

- Corresponding Receipt offered:

- Column (7) Gross Amount ( Gross receipt on which TDS is deducted)

- Column (8) Head of Income out of Income from business and Profession, Income from House Property, Income from Other Sources or Exempt Income

- Column (9) TDS credit being carried forward

Hello,

I would like to know whether we consider “transaction date” or “date of booking” in form 26AS for entering TDS deducted in ITR.

If we have to consider “date of booking” than what would we do with the entries where TDS deducted after 31/3/2021.

Thanks

please help me , i have foud three error, one enter gross receipt which is subject to tax deduction, select deduction year from dropdown, and enter tax deducted.give me reply

what gross amount I have to fill the corresponding receipt/withdrawal offered

in itr3 for ay 2022-23 error to tick radio button for tds2. there is no radio button but square button only. when ticked square button error continues.