Income Tax Return Form – 1 (Sahaj) is applicable to only Resident Individuals having Incomes from Salaries or Pension, One House property, Other sources and having total income upto Rs. 50 lakhs. The new ITR-1 form is not applicable to Non-residents and Residents but not ordinarily resident (RNOR).

The major changes in ITR-1 for the Assessment year 2018-19; Financial year 2017-18 are as below:

1. Income from Salary / Pension – Item No. 1: In the new form disclosure is required as per Form 16 under below heads:

- Salary (excluding all allowances, perquisites and profit in lieu of salary)

- Allowances not exempt

- Value of perquisites

- Profits in lieu of salary

- Deduction u/s 16

2. Income from One House Property – Item No. 2: Earlier net income from house property was required to be furnished, now details under below heads are required:

- Gross rent received/ receivable/ letable value

- Tax paid to local authorities

- Interest payable on borrowed capital

3.New Insertion Item No. 2 vi – Note : Maximum Loss from House property that can be set-off is INR 2,00,000.

4. New Insertion Item No. 4 – Note: To avail the benefit of carry forward and set off of loss, please use ITR-2

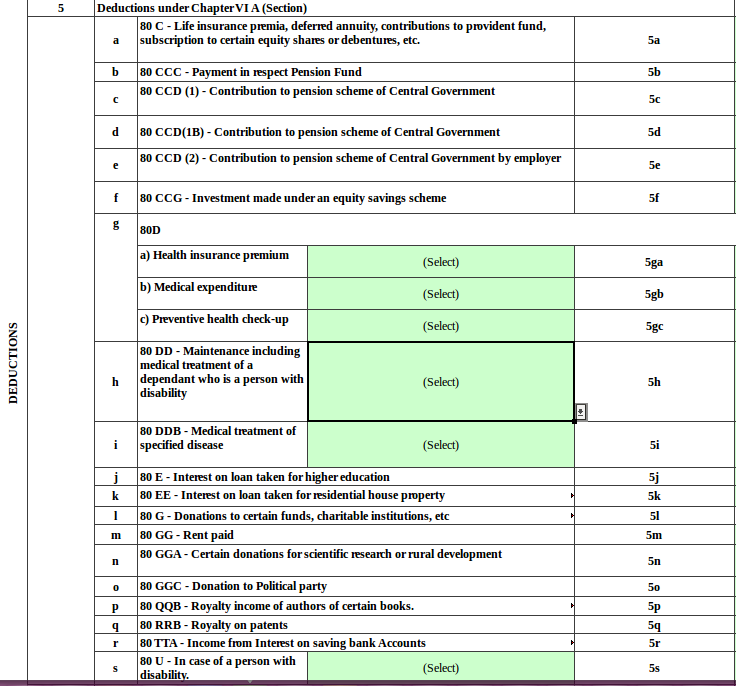

5. Deductions under Chapter VI A – Item No. 5 – Headings of Various deduction sections from 80C to 80U has been clearly specified. Section 80D has been further sub classified under:

- a) Health insurance premium

- b) Medical expenditure

- c) Preventive health check-up

6. Fee u/s 234F – Item No. 15d :

- A new field has been inserted to fill the details of late filing fees. Fees for filing of Income Tax Return after due date. Assessee shall now be required to pay the late filing fees mandatory under section 234F along with interest under section 234A, 234B and 234C before filing of return of income.

- Cases where the total income is less than Rs 5 lakhs, late filing fee is Rs 1,000.

- Cases where the total income is Rs 5 lakhs and above, if the income tax return is filed after the extended due date (August 31, 2018) but on or before the December 31, 2018, there will be late filing fee of Rs 5,000.

- Cases where the total income is Rs 5 lakhs and above, if the return is filed after December 31, 2018 but on or before the March 31, 2019, there will be late filing fee of Rs 10,000.

- After March 31, the returns cannot be filed.

7. Details of Tax Deducted at Source

- Item No. 19 TDS2 – Details of Tax Deducted at Source from Income OTHER THAN Salary [As per FORM 16 A issued by Deductor(s)] : Column for amount claimed in the hands of spouse if section 5A is applicable, has been removed.

- New Insertion – Item No. 20 TDS3 Details of Tax Deducted at Source [As per 26QC furnished by the Deductor(s)]

- Permanent Account Number (PAN) of the Tenant

- Name of the Tenant

- Amount which is subject to tax deduction

- Year of tax Deduction – 2017

- Tax Deducted – Amount of Tax deducted as per form 26AS

- Amount out of (column 5) claimed this Year – It means out of the total amount of tax deducted for the relevant year, how much is to be claimed in this assessement year. The remaining amount is allowed to be carried forward in future years. For example TDS deducted in FY 2017-18 is Rs. 200 and claimed in this year is Rs. 150, then amount in column 5 will be Rs. 200 and column 6 will be Rs. 150. Hence remaining Rs. 50 will be allowed to carried forward in next year.

8. Details of Tax Collected at Source – Item No. 22 TCS – Details of Tax Collected at Source [As per FORM 27D issued by the Collector(s)] : Column for amount claimed in the hands of spouse if section 5A is applicable, has been removed.

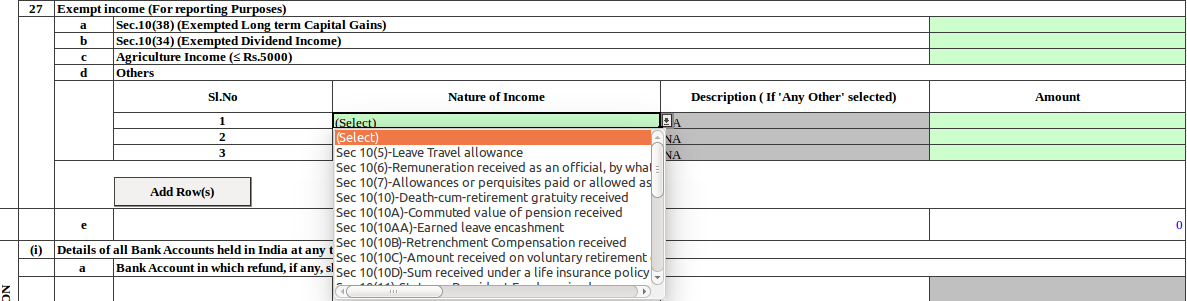

9. Exempt income (For reporting Purposes) – Item No. 27 (d)

- Headings of various exempted income under section 10 has been clearly specified.

- It has also specified list of Nature of Income to be selected from Allowance exempt under section 10

10. Under PART E – OTHER INFORMATION

- Requirement of Bank account details of Non-residents have been removed. Non-residents can no longer opt for the ITR-1 form. Only ITR-2 and ITR-3 forms are applicable to them.

11. Verification – “I am making this return in my capacity as” – Self or Representative

12. New Insertion – Item No. 28 Only if the return has been prepared by a Tax Return Preparer (TRP) below details will be required to be filled by TRP

- Identification No. of TRP

- Name of TRP

- If TRP is entitled for any reimbursement from the Government, amount thereof

For further assistance kindly contact us on +919825223809